by

by The lender will probably pull your credit report on one, two, or three of the credit reporting bureaus. These bureaus are TransUnion, Experian, and Equifax. Those bureaus generally receive similar information and your score on one of them will generally be quite similar to the score that you see on the other bureaus. If you’ve never seen your credit report, it basically lists everything that you have done financially in the recent past. This includes things like any accounts you have open like credit cards and mortgages but it

should also include things like auto loans and student loans. When they look at your credit report with these bureaus; they will also see your credit score. Credit scores can range between 300 and 850 points. They don’t necessarily have a “meaning”, it is just a number that consolidates all of your information and lets lenders judge you at a glance instead of having to dig into your specific numbers. This credit score acts as an indicator as to how risky it would be to lend money to you.

If you have a higher credit score, it would be considered better so an 850 could be considered as good as it gets while a 300 would be the bottom of the scale. It’ll be easier to borrow money if your score is higher.

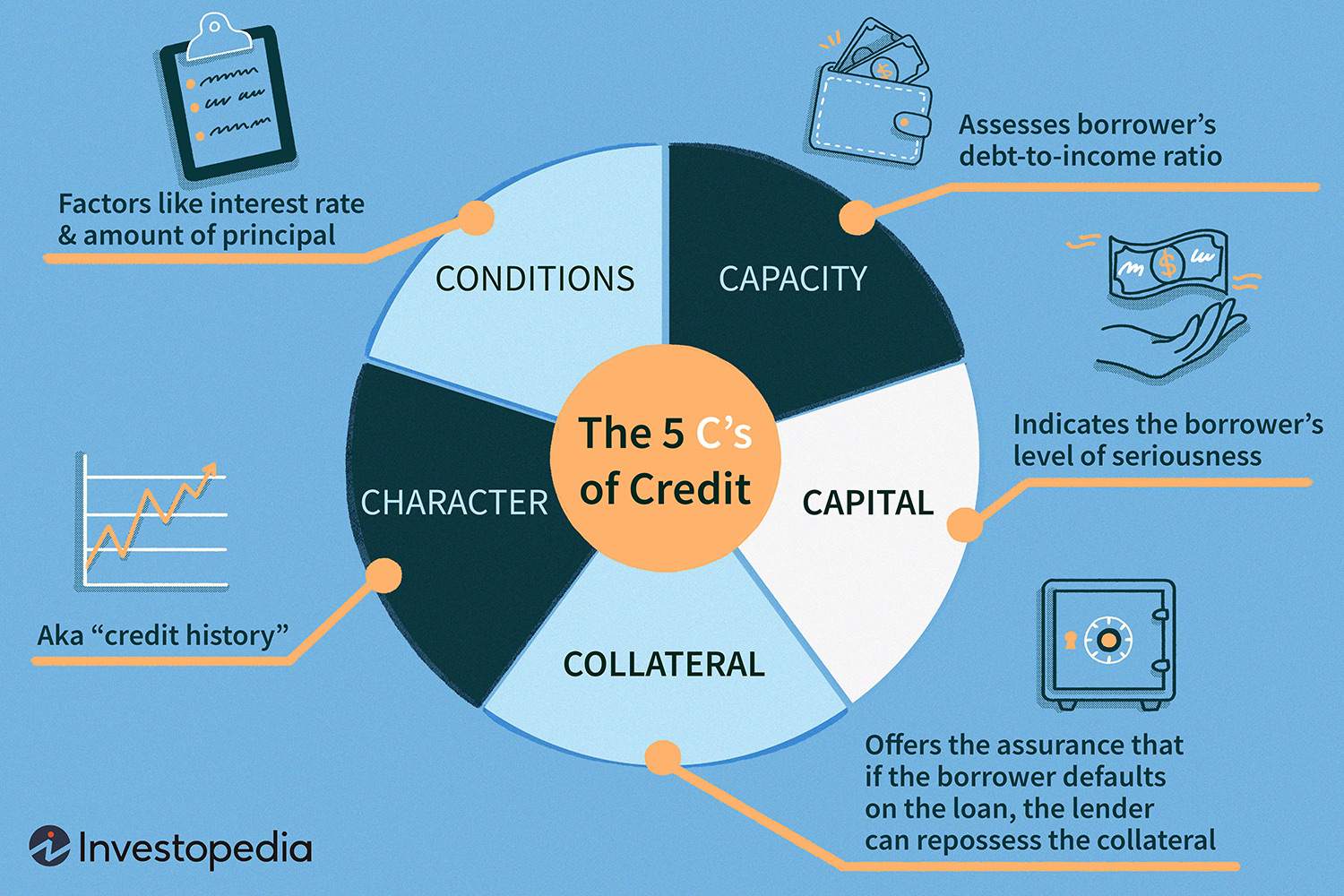

Capacity

Capacity refers to how well you have managed your credit in the past. This basically means that you have enough income to cover what your debt could be in the future. This also looks at how reliable your income is and what kind of income you receive. Basically, the lender needs to evaluate your ability to pay your debt if they loan you money. You should have a stable income and preferably the lender would see an income that is increasing as opposed to decreasing. If you have seasonal income, that may represent a slightly higher amount of risk to your lender because they won’t be as convinced that you will be able to afford regular debt payments year-round.

Collateral

Our next “C” word is collateral. This won’t be used in every kind of credit, but it is important to understand what it means and how it could be used in your lending application. If you are applying for any kind of credit that is secured, you may be asked to pledge an asset as collateral. If you are looking for a credit card, it would be a simple deposit that would be placed into a savings account. If you are buying something that is much more significant like a home equity product, you may have a hard time getting a loan based on some different factors. The lender will evaluate the value of your property and what you owe to figure out your equity.

Conditions

Taking care of your credit is one of the most important things you can do to better your personal financial life. If you want to reach your goals when it comes to finances, you had better learn how to take care of your credit and make sure that it stays healthy. If you have a credit score and a credit situation that is seen as “excellent” or healthy by creditors, you will have a much better chance of receiving financing in the competitive market that offers loans these days. If you suspect that your credit history has some negative marks, you can use the “4 C’s” to help you get yourself in a better position. It is important to keep a positive mindset when dealing with potential credit problems. These are situations that can be frustrating, especially when you have your heart set on something that seems like it may be out of reach due to your current situation. The number one thing to keep in mind is that you can take control of your situation and your life to achieve the things that you want to do. With that positive attitude in mind, let’s take a look at the “4 C’s” to help you understand what lenders are looking at when you apply for credit and how you can put yourself in a better position so that you can reach the goals you want to hit.

Credit History

This is probably the most obvious factor when it comes to things that lenders look at. Of course, lenders will want to know about your credit history. While it may not seem fair, the easiest way to judge what someone will do in their future is to look at their past experiences. The last C on the list refers to conditions. This applies to any loan or anything that you take out. The lender will want to have a say in how you are using your loan. There is a big difference between loans that are taken out as far as student loans, or for a new car. You can see how this would affect their decision because in the instance of student loans; the person they lend to is getting an education that should influence their future income in a positive direction. Every lender is going to insist on certain conditions that will only allow you to use your money in certain ways, there is no way around that.

Your Debt Matters More

The 4 C’s are not a guarantee that you will get everything you want. If you have a lot of debt, that is going to trump most of the 4 C’s. Lenders know that if you have a large amount of debt, it is going to decrease your ability to pay off new debt that they issue. It’s more than likely that you’ll need to deal with your previous debt instead of just getting more and more loans on top of what you have. You should consider getting information on a debt relief program if you are interested in increasing your ability to get new loans and keep a positive attitude as you can get out of this situation with solid focus.